The Best Way to Review Your Investment Portfolio

Most people don’t think of themselves as having an investment portfolio, but if you have a 401k, and perhaps a Roth IRA as well as a savings account for a long term goal, you most certainly do! Investing in the financial markets is an essential step towards building wealth and securing your financial future. However, the key to successful investing lies not just in making initial investment decisions but also in regularly reviewing and reassessing your portfolio.

If you are just starting out and need to pick some investments to build a portfolio, check out this blog post first.

Once you have done the hard work of picking investments for your accounts, how do you ensure that those choices are still performing year in and year out? If you are investing for yourself, you may be tempted to look at your accounts all the time. This is not necessary and short term market fluctuations can also lead to emotional decision making. Smart Sister Finance recommends reviewing your portfolio every 6 to 12 months to ensure it remains aligned with your goals, risk tolerance, and market conditions. More frequent review of long term accounts can actually be counterproductive.

So, what steps are needed to conduct a comprehensive annual review of your investment portfolio?

Review Your Investment Objectives:

Begin by revisiting your investment objectives. Are you investing for retirement, education, or a specific financial goal? An account that is growing for your retirement 30 years away should not be invested in the same way as a brokerage account that will be tapped to buy a house within 5 years. If your timeframe is longer, you have the ability to invest in some types of investments that might be more volatile, but have the tendency to grow faster over time. In your portfolio review, take a moment to reflect on your time horizon for each of your accounts, which will help you determine whether your current investments are on track or require adjustments.

Understand Your Risk Tolerance:

One way to define investment risk is the appetite to accept short term losses for larger long term gains. You can use this Schwab Risk Quiz to get a sense for your risk tolerance. As noted in the section above, your “timeline score” will be different for a retirement account vs a house down payment account, which may indicate investing more aggressively in accounts that will grow for many decades. Note that the asset allocation pie charts on page 4 of the Schwab Risk Quiz are guidelines. As with all aspects of personal finance, your risk tolerance is personal; there are no right or wrong answers.

Assess Your Asset Allocation:

At its most basic level, investing is spreading your money around to different “asset classes” such as stocks, bonds, cash, and alternative investments. This is also called diversification. The mix of investments is unique to you; ensure that your allocation is in line with your risk tolerance and investment strategy.

Asset allocation plays a crucial role in determining the risk and return profile of your portfolio. If you are heavily skewed towards US Large Cap and technology stocks, you may have enjoyed healthy gains in your accounts over the last 5 to 10 years, but also a lot of volatility. It is important to balance these investments with International stocks, bond funds or other choices which increase your chances of having solid portfolio performance no matter where we are in the economic cycle. Review the asset allocation pie charts from the Schwab Risk Quiz and realign your investments to the proportions of stocks, bonds, cash and alternatives that are right for you

Evaluate Your Individual Investments:

Analyze each investment within your portfolio. For mutual funds and ETFs (Exchange Traded mutual Funds), review the performance over time (3 year or 5 year returns), the gross expense ratio and the assessment of your investment against its benchmark.

You can use this simple worksheet to get organized. While this portfolio review tool references Fidelity, the same information can be found on any investment platform you use. What is most important is looking at longer term performance (3 year or 5 year returns) and how the investment you hold performs against its benchmarks.

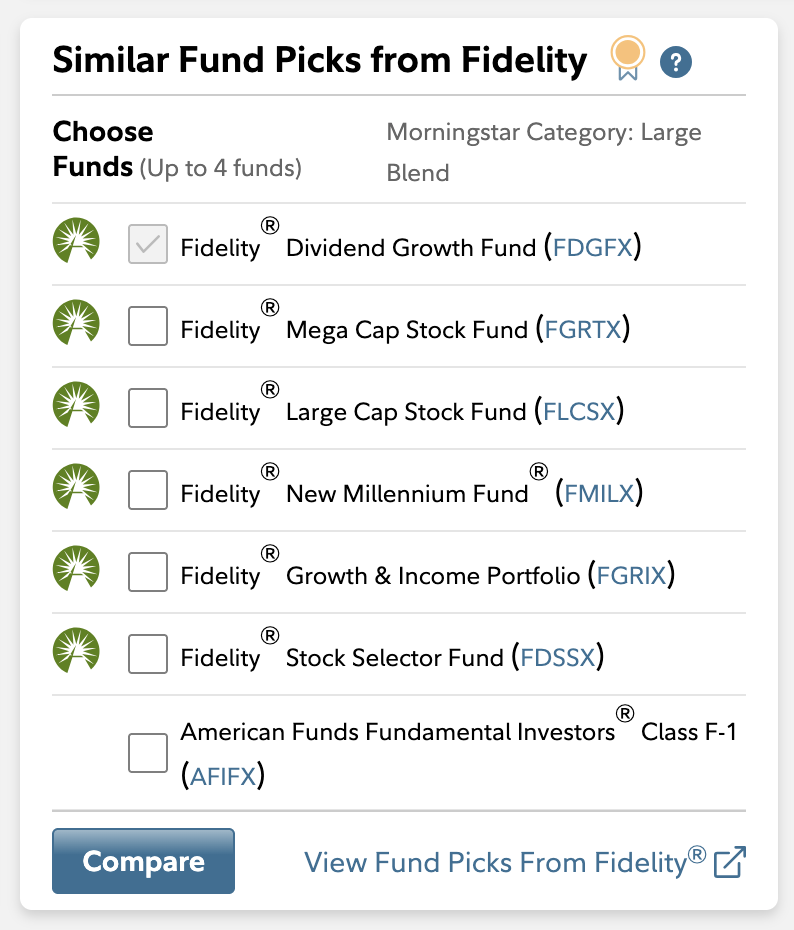

If you hold a mutual find or ETF that has consistently underperformed, look for alternative using your research tools, or start with the funds suggested by your chosen financial institution. Here is an example of Fidelity offering other mutual fund in the Large Blend (US Large Cap Blend) asset class:

Here’s an example from Fidelity. The Research Summary page for FDGFX shows these other investment options.

Assess whether each of your investments are meeting your expectations and if their fundamentals remain strong. Look out for any changes in management, competitive landscape, or industry trends that may impact their future prospects. Consider selling investments that no longer align with your investment goals or have consistently underperformed.

Adjust Your Strategy:

Based on your review, make any necessary adjustments to your investment strategy. This may involve rebalancing your portfolio, adding new investments, or eliminating underperforming ones. Set realistic expectations and remember that investing is a long-term commitment. Avoid making emotional decisions based on short-term market fluctuations.

Rebalancing is the process of reducing or increasing some investment holdings to bring you back in line with your chosen asset allocation. In an IRA or other tax-advantaged account, you can easliy make adjustments or swap investments with no tax implcations. In a Brokerage or other investment account, be aware that if you sell positions you may have a capital gain or loss. Capital gains can be netted against capital losses and are subject to a tax of 15% when you file your taxes. One way of slowly reducing an investment position is to turn off the reinvestment option. Any dividends or capital gains will accumulate in your account as cash for you to reinvest in another asset class, fund or stock.

Stay Informed:

If you have significant investments in riskier parts of the market such as cryptocurrencies, it is important to stay updated on the news and trends in that sector of the market. The same holds true if you are building a conservative portfolio that relies on producing investment income. Fluctuations in interest rates and inflation may require adjustments to ensure your income expectations are met. Use reputable financial publications and websites for news and analysis and check multiple sources if needed. Being well-informed will help you make better decisions during your portfolio review.

By following these portfolio review steps, you can gain valuable insights into the performance of your investments, make informed decisions, and position yourself for long-term success. As always, choose the mix of investments for each of your accounts that feels right to you and know that you can adapt and shift your portfolio as your circumstances and the market evolve.